- By: Prakul Thadi

- NCLAT

- Dec 13

- Comments (0)

MONEY RECEIVED AS LOAN WITH REGARD TO FUTURE SUPPLIES OF MATERIAL BE TREATED AS FINANCIAL DEBT: NCLAT

CASE SUMMARY

Gaurav Agrawal, Director M/s. Albus India Ltd. – Appellant vs M/s Tuf Metallurgical (P) Ltd. & M/s Albus India Ltd. – Respondents (Company Appeal (AT) (Ins) No.212 of 2019)

Order dated September 4, 2019 by Justice S.J. Mukhopadhaya (Chairperson), Justice A.I.S. Cheema (Member – Judicial), Kanthi Narahari (Member – Technical) 1. Issue in Consideration Whether the money received as loan with regard to future supplies of material be treated as financial debt? 2. Brief Facts of the Case- M/s. Tuf Metallurgical (P) Ltd. (the “Financial Creditor”) filed application for initiation of corporate insolvency resolution process (the “CIRP”) under Section 7 of the Insolvency and Bankruptcy Code, 2016 (the “IBC”) against M/s. Albus India Ltd. (the “Corporate Debtor”) before the National Company Law Tribunal, New Delhi Bench (“NCLT”).

- The Application was filed by the Financial Creditor claiming that there was debt and default of Rs.10,29,56,582/-.

- The Financial Creditor claimed to have disbursed Rs.2,51,44,385/- in instalments between October, 2016 to March, 2017 to the Corporate Debtor by way of financial assistance which was repayable by June 30, 2017 or on demand with interest @ 24% per annum. A “Share Pledge/Finance Facility Agreement” dated April 4, 2017 (“Agreement”) was executed, and the limit was extended to Rs.5 Cr. (“Loan-1”).

- On April 17, 2017, demand Promissory Note was executed by one of the Directors of the Corporate Debtor accepting the liability of the financial loan for and on behalf of the Company as well as in his personal capacity.

- The Board of Directors pledged shares worth Rs.5 Crores and on August 31, 2017, Albus Conserves Pvt. Ltd. – a sister concern of the Corporate Debtor offered security of equitable mortgage to the Financial Creditor.

- There was a default in payment of debt and the Financial Creditor issued a Demand Notice dated February 23, 2018.

- In addition to the above, a sum of Rs.1,13,46,653/- was also due from the Corporate Debtor to the Financial Creditor payable on account of release of 18.761 MT of Graphite Electrodes from the Vizag Port which was paid by the Financial Creditor on behalf of the Corporate Debtor (“Loan-2”). The Corporate Debtor issued four (4) cheques in response to the legal notice but the same got bounced. Thus, the Financial Creditor claimed that there were two loans as above.

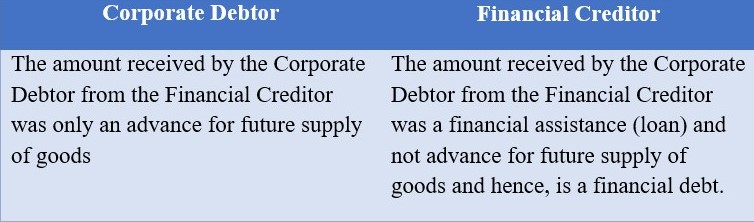

- The Corporate Debtor opposed the admission of the application for CIRP by stating that it had trade relations with the Financial Creditor and the Financial Creditor had been purchasing Carbon Ferro Chrome which is produced by the Corporate Debtor. According to Corporate Debtor, the money received from the Financial Creditor was with regard to supplies of future material and there was no disbursement of amount against time value of money to qualify as financial debt under the IBC.

- After hearing both the parties, the NCLT had held that it is a financial transaction and such amount fits within the definition of financial debt u/s 5(8)(f) and hence, vide its order dated January 2, 2019, admitted the application filed by the Financial Creditor u/s 7 of the IBC.

- The NCLT has admitted the application for CIRP filed by Financial Creditor vide its order dated January 2, 2019.

- Aggrieved by the order, Mr Gaurav Agrawal, Director of theCorporate Debtor preferred an appeal before the National Company Law Appellate Tribunal (NCLAT).

- It was argued by the Appellant that in the year 2016, the Corporate Debtor informed the Financial Creditor of its inability to supply raw material owing to its financial difficulty.

- In order to tide over the financial crisis of the Corporate Debtor, the Financial Creditor offered advance payments for future supplies of material and as the supply was taking more time, the Corporate Debtor executed Promissory Notes only as a measure of security and not otherwise.

- According to the Appellant, as per the terms of the Agreement, the Financial Creditor was to have first right to procure from the Corporate Debtor on priority basis a minimum of 500 MT of Low Carbon Ferro Chrome per month and if the Corporate Debtor supplied material directly to third parties, the Financial Creditor was entitled to a commission of 3 – 5 percent of the billed amounts and hence, Loan-1 was wrongly being stated to be financial debt.

- With respect to Loan-2, it was argued that it was nothing but payment of demurrage charges (a charge for detaining a ship, freight car, or truck).

- The Financial Creditor argued that it had advanced Rs.2,23,14,261/- and there was further loan of Rs.5 Crores. The letter dated April 5, 2018 issued by the Corporate Debtor was referred, wherein the Corporate Debtor acknowledged the Financial Creditor towards withholding of the material at Vizag Port on behalf of the Corporate Debtor.

- The Financial Creditor also referred to reply of the Corporate Debtor dated March 5, 2018, wherein it was pointed out that the Corporate Debtor sought for time and accommodation without denying the liability.

- It was finally submitted that the transaction was clearly a transaction of financial debt and that application filed u/s 7 of the IBC was rightly admitted by the NCLT.

It can be observed from above that the interpretation of the Agreement entered between the parties was crucial in determining the case. Hence, utmost care shall be taken while drafting of such complex agreements containing both pure loan covenants as well as other performance related covenants.