- By: Sharath Chandra

- Deposits

- Jun 22

- Comments (0)

DISSECTING DEPOSITS : UNDER COMPANIES ACT, 2013

Deposits contribute as one of the most important sources of debt funding for many Companies, despite its size. Deposits provide companies with cost-effective means of finance, and the depositors with a higher rate of return on the investment, simply by eliminating the middlemen in the form of Banks or Financial Institutions.

To better regulate the acceptance and repayments of Deposits, and to avoid malpractices by the Companies accepting deposits, Companies Act, 2013 has come up with a rigid set of provisions and rules, binding such companies. Such rules and regulations have been, and still are a nightmare for many of the Companies and even among the professionals. This is an attempt to present the concept of deposits in a relatively simpler way.

What is a Deposit?

To understand the rules and regulations surrounding Deposits, it is imperative and of utmost importance to understand the meaning of the word ‘Deposit’. What constitutes to be a deposit and what doesn’t.

Sec 2(31) of Companies Act, 2013 defines deposits as:

‘deposits’ includes any receipt of money by way of deposit or loan or in any other form by a company, but does not include such categories of amount as may be prescribed in consultation with the Reserve Bank of India.

And, as prescribed by Rule 2 (1) (c) of Companies (Acceptance of Deposits) Rules, 2014 Deposit includes receipt of money by way of deposit or loan or in any other form, by a Company but doesn’t include the following amounts:

|

The following amounts shall not be treated as Deposits (Important ones emphasised) |

|

Amount received from: · Central / State Government / · Local Authority / · Statutory authority formed under State/ Central Law |

|

Amount received from any other person, whose repayment is guaranteed by Central / State govt; |

|

Amounts received from: · Foreign Governments, Foreign or International banks, · Multilateral financial institutions (ADB, CDC, IFC, IBIFR, etc.,) · Financial institutions owned by Foreign Governments, · Foreign export credit agencies, · Foreign Collaborators, · Foreign body corporates and foreign citizens, · Foreign Authorities or Persons resident outside India (All subject to provisions of FEMA,1999) |

|

Loan/ Facility- received from · notified Banking Institutions · Public Financial Institutions · Regional Financial Institutions · Insurance Companies · Scheduled Banks |

|

Amounts received by issuance of Commercial Paper |

|

Any amount received by the Company from another Company |

|

Amount received pursuant to any offer made in accordance with provisions of Companies Act, 2013, such as Share Application Money, etc., unless amount is appropriated for allotment of such securities. (If securities are not allotted within 60 days of receipt, it must be within in 15 days completion of 60 days; Any other adjustment of such money shall not be treated as refund) |

|

In case of a Private Company: Any amount received from a Director / Relative of Director. (This amount shall not be borrowed amount; Company shall disclose amount so accepted in Board’s Report) |

|

Any amount- Raised by issue of Bonds/ Debentures (Provided they are secured by First/ Pari Passu Charge on Assets (Excluding IPRs)) (Value of bonds/ debentures < Market value of assets charged) Assessed by RV |

|

Compulsorily Convertible Bonds/ Debentures (within Ten years) |

|

Unsecured Non-Convertible Debentures (Provided they are listed on a Recognised Stock Exchange) |

|

Amount received from employee (As non-interest-bearing deposit) (Not exceeding annual salary) |

|

Any non-interest bearing amount received and held in trust |

|

Amount received in course of Business / for purposes of Business: · As advance for goods/ services (Provided that they are appropriated against supply of goods /services within 365 days from receipt.) · as advance, in connection with 2[consideration for an immovable property] under an agreement or arrangement · as Security deposit for performance of contract · as advance received under long term projects for supply of capital goods · as advance taken towards warranty or maintenance contract as per written agreement · as advance- allowed by sectoral regulator · as advance- for subscription of publications (print/electronic) |

|

Amount brought in by Promoters as unsecured loan, due to stipulation imposed by Lending Financial Institution / Bank provided that: · Loan is provided to meet stipulation of Bank / Lending financial institution · Loan is provided by Promoters and/or relatives of promoters · The amounts are kept only till the loans from Banks / Lending institutions are repaid. |

|

Any amount received by a Nidhi Company. |

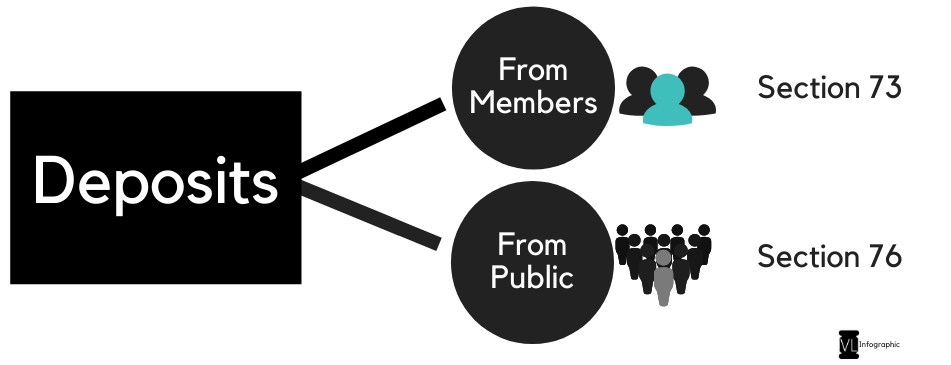

Modes of Acceptance of Deposit

Section 73 of the Companies Act, 2013 allows companies to accept deposits from its Members, subject to passing of an Ordinary Resolution by the Members at an EGM. And every deposit accepted as such shall be repaid duly in accordance with terms and conditions of the acceptance of such deposits.

Section 76 of the Companies Act, 2013 allows the “eligible” companies to accept deposits from persons other than its members, provided that such eligible company obtains Credit Rating from a recognised Credit Rating Agency every year during the tenure of deposits, and provided that the deposits are secured by creating a charge over assets of the Company.

Eligible Company means a Public Company, having net-worth > Rs. 100 Crores / Turnover > Rs. 500 Crores, and has obtained prior consent from its members vide a special resolution for raising the deposits.

Limits on the amounts which can be raised as Deposits

The Limits on amount of deposits that can be raised for different classes of companies can be classified as follows.

|

Source |

Company |

Type |

Sub Type |

Limit |

|

From Members (U/s 73 (2)) |

Private |

Start-up |

|

No limit, for 5 years from the date of Incorporation.

No need to comply with procedure under provisions of 73 (2) (a) to (e). |

|

Other than Start-up |

· Not a Subsidiary/ Associate of any company · Borrowings from Banks & Financial Institutions / Body Corporates is less than twice of Paid up Capital or Rs. 50 Crores (Whichever is less) · It has not defaulted in repayment of any such borrowings aforementioned |

No Limit.

No need to comply with procedure under provisions of 73 (2) (a) to (e). |

||

|

Any other Company |

Upto 100% of Paid up Capital + Free Reserves + Securities Premium Account. (Notification GSR 464- 5th June 2015) |

|||

|

Public |

IFSC Public Company |

|

Upto 100% of Paid up Capital + Free Reserves + Securities Premium Account |

|

|

Eligible Public Company |

|

Upto 10% of Paid up Capital + Free Reserves + Securities Premium Account |

||

|

Others |

|

Upto 35% of Paid up Capital + Free Reserves + Securities Premium Account |

||

|

From Public (U/s 76 (1)) |

Public |

Eligible Public Company |

|

Upto 25% of Paid up Capital + Free Reserves + Securities Premium Account |

|

Ineligible Public Company |

|

NIL |

||

|

Government |

Eligible Government Company |

|

Upto 35% of Paid up Capital + Free Reserves + Securities Premium Account |

|

|

Private |

|

|

NIL |

Conditions for acceptance of deposits

· Minimum term of deposits shall be 6 Months and Maximum term shall be 3 years.

· Minimum term can be reduced to 3 Months if the deposits don’t exceed 10% of Paid up Capital + Free Reserves + Securities Premium Account.

· Rate of interest should not be above maximum rate of interest or brokerage prescribed RBI for acceptance of deposits by NBFCs.

· Eligible company shall obtain credit rating from approved credit rating agencies atleast once in an year, which shall be filed along with DPT-3.

· The rating obtained above shall not be less than the standard approved by RBI w.r.t Fixed deposits with NBFCs.

Circular inviting deposits and its contents (Rule 4)

· Company shall issue circular in form DPT-1:

– through registered post / speed post/ electronic mode- in case of invitation of deposits from its Members.

– through publication in English and Vernacular Newspapers (State level) and on its website- in case of eligible companies inviting deposits from public.

· DPT-1 shall be annexed with a certificate from Statutory Auditor stating that the Company has not defaulted in repayment of deposits/ interest on deposits.

· Approved copy of the circular signed by majority of Board of Directors shall be filed with ROC atleast 30 days prior to the dispatch/ publication.

· Such circular issued shall be valid up to six months from the closure of financial year in which it is issued/ date of AGM / due date of AGM (whichever is earlier), and new circular shall be issued every year for accepting the deposits (continuously).

Secured Deposits

· The Company inviting secured deposits shall appoint a deposit trustee.

· The Company shall create security by creating a charge on its assets in favour of the deposit trustee so appointed.

· The value of assets on which the charge is created in favour of deposit trustee shall be equal to or more than the deposits accepted by the company and interest payable thereon.

· The deposit trustee shall be responsible for conducting the meeting of deposit holders upon requisition or whenever necessary.

Other Conditions

· Application filed by deposit holders shall contain a declaration that the deposits are not made out of the borrowed monies.

· Deposit holder may nominate any other person, with whom the title of the deposit shall rest in the event of death of the deposit holder.

· Upon acceptance/ renewal of deposits, the company shall issue a Deposit Receipt to the deposit holder, within 21 days from receipt of Money.

· Companies accepting deposits shall create a reserve called Deposit Repayment Reserve with any scheduled bank, to which the Company shall transfer twenty percent of the deposits maturing every year on or before 30th April every year. This reserve shall be used exclusively for the repayment of deposits. · The company accepting deposits shall maintain a register of deposits containing particulars of deposit holders.

· If the deposit is repaid on demand, before the expiry of the term of deposit, the rate of interest payable on such repayment shall be reduced at least be one percent.

· Every company, on or before 30th June of every year shall file e-form DPT-3 showing the particulars of Deposits, and the particulars of amounts not considered as deposits.

· Penal interest rate shall be 18% in case of delay in repayment of deposits.

· Any misstatement or fraudulent activity of the company or any person in charge shall be punishable as per the provisions of section 447 of the Companies Act, 2013.